Why is Europe All-In on Ukraine?

How the EU Uses War to Stave Off Economic Decline

The German economy is in recession. Manufacturing has imploded, particularly in the crucial automotive sector, which has shed hundreds of thousands of jobs since 2022, and lost a staggering third of its production volume since 2018. August saw the biggest drop in industrial output in more than three years, over four times the decline analysts expected. The crucial machinery sector has dropped 22% since the pre-covid period, with a 5.6% drop expected this year alone. In recent months, massive declines have occurred in the pharmaceutical, electronic, energy, construction, and hospitality industries.

A brutal combination of energy price increases, increased regulation, tariffs, competition from China, and government policy have crushed Germany, which underpins the European economy. The supply chains for its manufacturing sector typically stretch across the entire EU, and the controlled demolition of its productive output is having ripple effects across the continent.

The German solution to this is debt – lots of debt. German borrowing has been extraordinarily reserved for a Western state ever since the “debt brake” amendment passed by the first Merkel cabinet came into effect in 2016, limiting deficit spending to 0.35% of GDP. In 2022, then Chancellor Olaf Scholz successfully led an amendment to the rule that allowed the creation of a €100 billion defense fund immune from the brake. In spring of this year, Scholz and incoming Chancellor Friedrich Merz agreed to another amendment to exempt defense spending over 1% of GDP. Over challenges from the AfD, FDP, and Die Linke, the amendment was passed in late March. In both cases, the war in Ukraine was the explicit rationale for subverting Germany’s debt limits.

With deficit defense spending now unrestrained by its constitution, the German government announced earlier this year that it plans to double its current levels of defense spending over the next five years. $761 billion will be spent by the end of 2029. More than half – $469 billion – of this total will be funded through new debt. Net German government borrowing already more than doubled this year, increasing from $38 billion in 2024 to at least $95 billion by the end of 2025. Included in the 5 year spending plan is at least $10 billion in direct aid to Ukraine.

While it may seem imprudent for the German government to attempt to revamp the Bundeswehr and simultaneously fund a proxy war in the midst of a historic economic decline, there is a certain logic at play. In this piece, we’ll explore how EU economies benefit from the continuance of the war in Ukraine, and how they use the war to offset the effects of deindustrialization.

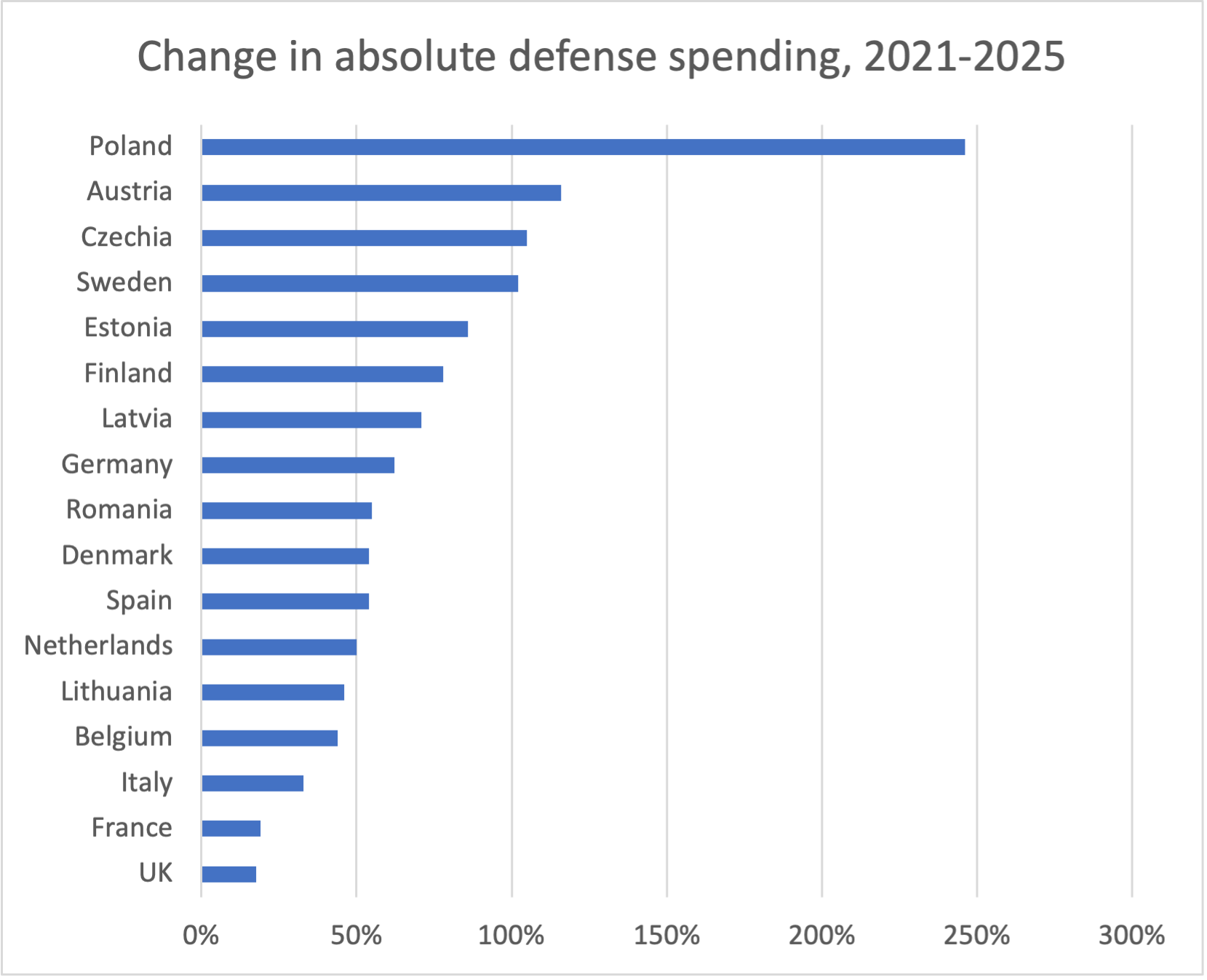

EU defense spending since the war began has surged by over 50%, increasing by nearly $150 billion a year from 2021-2025. The only EU state which hasn’t seen double-digit growth in defense expenditures since 2021 is Greece, which modestly decreased its spending.

These figures do not include the $70 billion in military “aid” to Ukraine given during this period, some of which is considered an investment instead of an expenditure, because it often comes in the form of loans. Ukraine currently owes $117 billion in debt to external creditors, with $50 billion of this figure being to EU institutions, and the remainder being to international lenders through which the EU has significant exposure, like the IMF and World Bank. In total, the EU has provided just under $200 billion in assistance to Ukraine, and another $170 billion in assistance to Ukrainian refugees residing within the EU.

Taken in cumulative terms since the beginning of the war, and projected forward in line with planned spending and debt increases across the EU, the war in Ukraine is the justification for an enormous injection of borrowed cash into the European economy roughly at the same scale of the $700 billion emergency bank bailout during the 2008 US financial crisis. Unlike the 2008 bailout, however, this project has gone largely unremarked upon – being laundered through messaging around “peace through strength” or the “defense of democracy,” rather than being taken as an emergency measure to stave off economic decline.

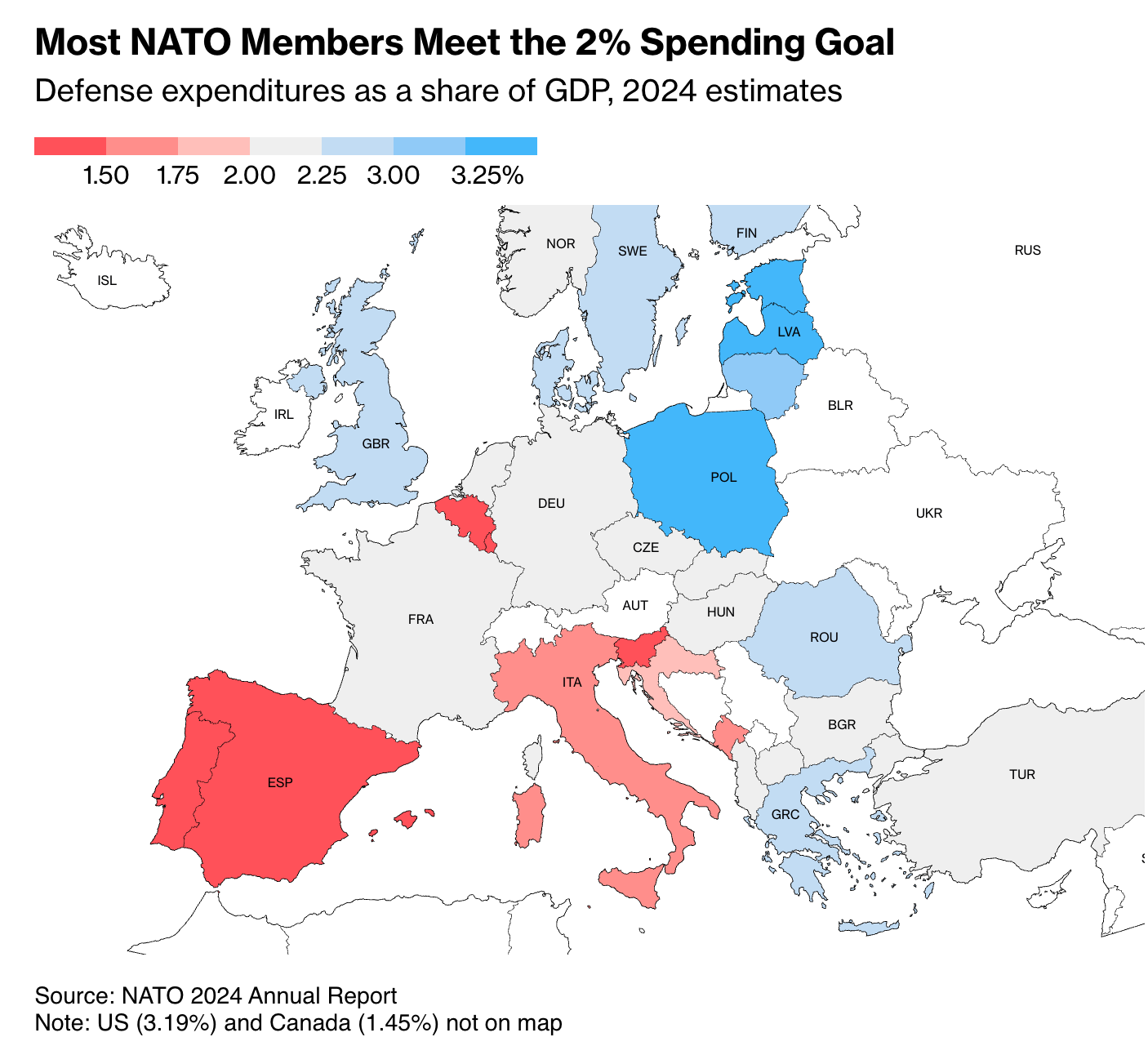

While these numbers may sound astronomical, the EU is just getting started. In June, NATO collectively agreed to meet Trump’s requested target of 5% of GDP on defense spending. All NATO member states are on track to hit the initial 2% target by the end of this year, meaning spending will more than double by 2035. Spending specifically for Ukraine will count towards the target.

Out With the Old

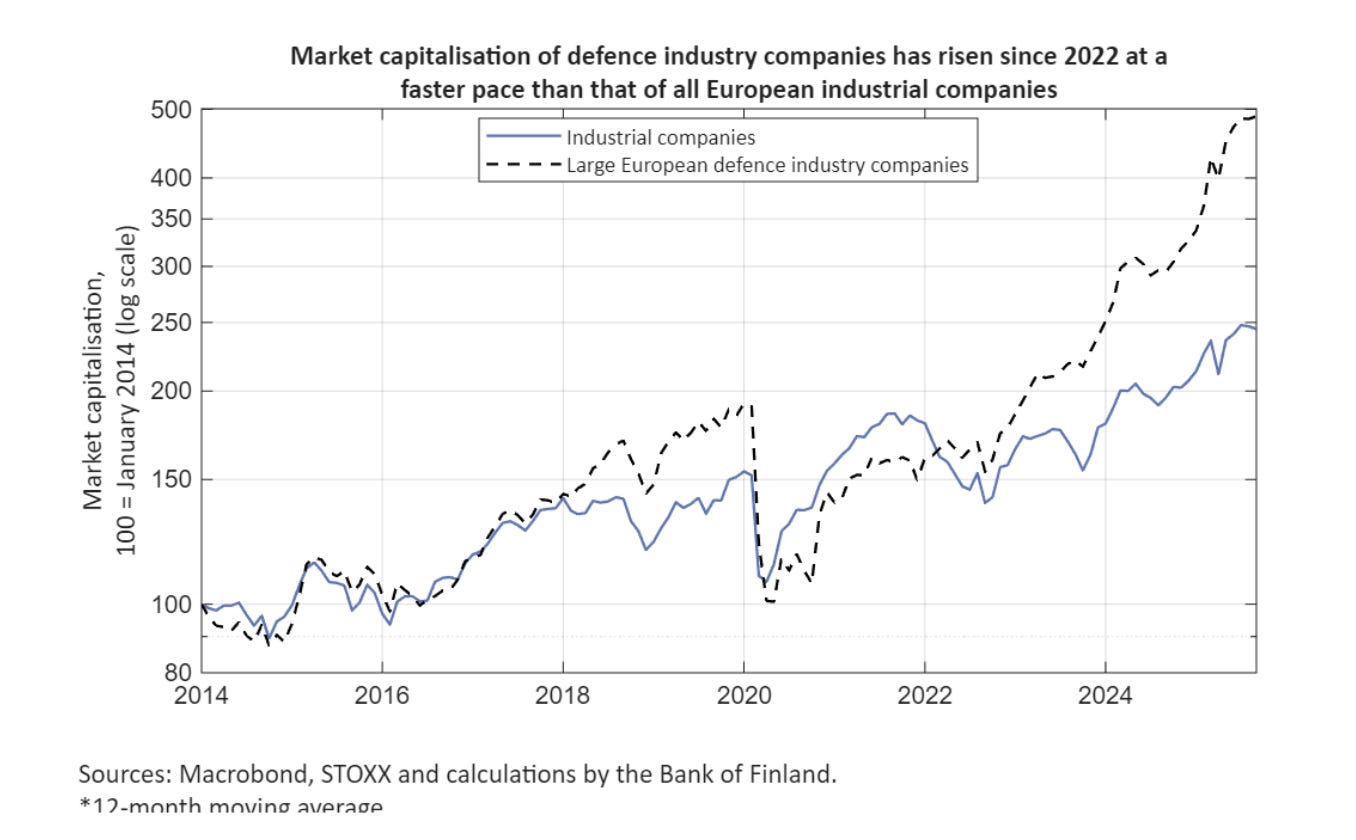

Nowhere is the substitution of defense spending for typical economic activity more obvious than in Germany. As the share price of automakers like Porche (-41% since IPO), Mercedes (-21%) and Volkswagen (-51%) have been stagnant or declined dramatically since the war began, the German defense industry has surged. Rheinmetall, Germany’s second largest defense contractor, has seen its stock grow 2522% in value since 2020, and Airbus, Germany’s largest, has jumped 224%. The STOXX index, which tracks Europe’s total aerospace and defense market, has posted gains of 229% since February 2022.

This has resulted in an interesting phenomenon – German automotive factories being converted to defense sector production.

“So we think it’s very important for the German industry and for us to find new markets. And where are new markets? Well, government has committed a lot of new funding for defense. We are quite close to what defense industry needs, so it’s very obvious for us to look to this market.” Marin Buchs, JOPP group (NPR)

Automotive suppliers across Germany have avoided closure by switching to the production of military drones, engines for armored vehicles, and artillery barrels. Rheinmetall, which itself makes automotive components for the civilian market, has begun to convert two of its plants to defense products, and plans to purchase a VW plant that once employed 2,300 people but shut down in 2024. Rheinmetall’s automotive division has seen consistent declines in revenue while its defense divisions post triple digit operating profit increases. German/French defense group KNDS announced a similar plan to retool an east German plant which once made train locomotives to instead manufacture Puma and Leopard 2 armored vehicles. KNDS is planning an IPO, while Thyssenkrupp prepares to spin off its naval defense subsidiary TKMS.

The plans of European defense contractors universally hinge on guarantees for purchase minimums from their respective governments. Rheinmetall requested a contract for at least 1,000 armored vehicles in order to move ahead with their proposal to purchase the defunct VW factory. While building out the Bundeswehr will require vast quantities of new vehicles, there’s no better justification for large contracts than the war in Ukraine. The conflict has vacuumed up tens of thousands of infantry fighting vehicles, MRAPs, armored cars, and tanks, and because much of this material is destined to be destroyed, there will always be a need for more. Rheinmetall’s order backlog at the beginning of the year stood at $65 billion – six full years of sales at current levels.

The success of the defense industry amidst the decline of the automotive industry is the result of a simple asymmetry. While automakers compete in a relatively open market, defense contractors do not. Concerns like the costs of energy and labor create insurmountable obstacles to manufacturing within Europe, because consumers have the ability to select cheaper options from manufacturers in places like China. With real earnings for the German population still below pre-2022 levels, access to cheap overseas goods is essential to prevent a precipitous decline in quality of life.

The defense industry does not need to play by these rules. Arms deals don’t adhere to free trade principles, and are often negotiated through a combination of political pressure, bribery, and government subsidies. Input costs, like energy, are largely irrelevant, and purchase price is not a significant concern. Nowhere is this more true than in Ukraine, where any notion of free market competition is nonsensical. To understand this, we’ll analyze how procurement contracts between the AFU and the European defense sector work in practical terms.

Grants

There are three overlapping types of military aid to Ukraine: grants, loans, and the “Danish Model.” Germany issued a €5 billion aid package to Ukraine in the form of a grant in May of this year, drawing the money out of their defense budget. This package unlocked major contracts that had been in the works for months, including one with the German firm Helsing to supply thousands of HF-1 and HX-2 attack drones. Founded in 2021, Helsing is Europe’s most valuable defense tech startup, and is currently valued at over €12 billion. The company is well connected and funded – its co-founder and co-CEO Gundbert Scherf spent two years at the German defense ministry under EU commission president Ursula von der Leyen. It has competed directly against US defense contractor Anduril, winning a contract to work on an update of the Eurofighter Typhoon’s software package.

After delivering hundreds of drones from 2022 to 2024, Helsing had already started production of the HX-2 before the German government funds were made available, and signed a provisional contract with the Ukrainian Ministry of Defense to deliver up to 10,000 units. The earlier HF-1, which Helsing is in the process of delivering 4,000 units of, is manufactured as the deliberately cheap (its frame is plywood) AQ 100 Bayonet by a tiny Ukrainian defense contractor called Terminal Autonomy. The system is then transferred to Helsing, which modifies the drone with updated electronics and Helsing’s targeting software, called Altra.

The HF-1 has been the subject of enormous criticism from the Ukrainians. In March, AFU serviceman and drone expert Okeksandr Karpyuk posted a lengthy diatribe attacking the HF-1 for its “crap” explosive payload and “primitive” targeting system. NATO officials have agreed, saying Helsing’s drones have more problems than comparable models.

“We’re talking about a product that is made of cheap components and is being marketed as cutting-edge technology, I can assure you, because I disassembled it. Such a product is worth at most 100,000 hryvnia (€2,200). And it costs €16,700, which is exorbitant.” - Oleksandr Yarmak, Unmanned Systems Force, AFU (Bloomberg)

Helsing’s fundamental business model with the HF-1 is to take an exceptionally cheap, Ukrainian-made drone – once listed by Terminal Autonomy for €1,800 prior to Helsing’s upgrades, though this has now been removed from its website – upgrade its electronics and software, increase the price by a factor of up to 10x, and bill the German government for it.

The HX-2 fills a similar role to the Russian Lancet, but likely costs at least twice as much. The founder of a competing German drone startup called Quantum Systems, Florian Seibel, publicly accused Helsing of lying about the HX-2’s range and payload, and offered a €100,000 donation to Helsing’s charity of choice if they could publicly prove to meet them. A threat of legal action by Helsing forced him to sign an NDA a day later.

The negative feedback has yet to have a visible impact on Helsing’s ability to turn a profit or sell its products. Co-founder Torsten Reil suggested that 100,000 HX-2’s could form a “drone wall” to protect NATO’s eastern border with Russia, forever deterring a land invasion. EU leaders like von der Leyen and Lithuanian prime minister Andrius Kubilius have publicly echoed the concept, estimating covering Poland and the Baltics would cost approximately $1 billion (enough for tens of thousands of HX-2s). The contact to supply the AFU with the HX-2 is in progress.

The case of Helsing is a microcosm of how the European defense manufacturing industry can thrive, even while other forms of manufacturing become ever more unviable. For Helsing, market demand is not an issue, as Ukraine has unlimited need for munitions. Competition isn’t a problem, because deals are made as a matter of government policy rather than through consumer choice. Pricing is arbitrary, as the government subsidizes all purchases. High energy prices and labor costs may eat into an already sky high profit margin, but if you’re as clever as Helsing’s founders, you let the Ukrainians do the manufacturing. It’s doubtful that Helsing would be able to bring a product to market that could compete on price or capability without the peculiarities of the defense sector, or during peacetime.

Helsing has less than a thousand employees. The defense tech startup model and even the much larger scale shifts from automotive to defense manufacturing from firms like Rheinmetall have so far not be able to offset the employment decline in other manufacturing sectors. While each week seems to bring new announcements of mass layoffs of tens of thousands of German industrial workers, the defense industry has only made marginal hiring increases, adding around 15,000 jobs since 2022.

Helsing has used its profits to go on a buying spree, purchasing German aircraft manufacturer Grob in June, Australian underwater drone manufacturer Blue Ocean, and forming a strategic partnership with ARX robotics for make unmanned ground vehicles.

Loans

In March, the UK announced an exceptionally large $2.1 billion deal to supply Ukraine with 5,000 Thales lightweight-multirole missiles (LMM), also known as Martlets. The deal was a boon to Thales UK, a subsidiary of Thales Group, which is partially owned by the French government. The contract will eventually triple the output of the Thales facility in Belfast. A purchase order of this size is unusual, and the Ukrainians would never be able to afford it without help.

In July of 2024, the UK and Ukraine signed the Defense Export Support Treaty. Under the terms of the treaty, the Ukrainians would be able to draw $4.6 billion in financing for military equipment from the UK Export Finance (UKEF), an export credit agency under the UK government. The UKEF’s mandate is to support the British economy by helping firms win business, providing insurance, and most importantly issuing loans for domestically produced goods.

The ministerial department has faced criticism as a form of subsidized bribery, and historically up to 50% of its business has been in support of arms deals. The LMM deal alone will consume almost the entirety of the Defense Export Support Treaty, due to underwriting overheads, making the LMM deal one of the largest single bilateral loans for procuring a specific weapon system since the beginning of the war. It’s a new level for the UKEF, which typically doesn’t sign deals valued at even half as much. The British parliament determined that the UKEF’s typical risk standards – which require it to return a modest profit – could be bypassed when lending money to Ukraine. Under the terms of the financing agreement, the Ukrainian debt servicing responsibilities will be “at a standstill” until 2027, and the full repayment term won’t mature until 2037.

In practical terms, the deal works as follows: First, the Ukrainians secure the $4.6 billion loan from the UKEF, which is backstopped by the British taxpayer. Next, the UK MoD’s procurement arm, Defense Equipment & Support, places the order “on behalf” of the Ukrainians, and the money is transferred from UKEF to Thales. The Ukrainians pay interest on the loan, and receive the missiles. The contract is for a term of nineteen years, meaning Thales has no responsibility to deliver the final batch of the order until 2044.

The British government has proudly claimed that the deal will create up to 200 jobs in Northern Ireland, and preserve the jobs of the hundreds of workers already employed by the Thales factory in Belfast. At a liability of $23 million per job created, the return on investment here is questionable, especially as the UK manufacturing sector has shed 57,000 jobs since the war began. For Thales, with its $53 billion market cap, the benefit is more clear. In the months leading up to the deal its stock price increased by nearly 100%.

The UKEF’s counterparts in other EU states include Italy’s SACE, France’s Bpifrance, Denmark’s EIFO, Finland’s Finnvera, and Belgium’s Credendo. All have issued loans to Ukraine.

The Danish Model

Denmark, which has little defense production of its own, has pioneered a unique approach to funding Ukraine’s war effort. Rather than loaning Ukraine money to purchase European hardware, Denmark issues loans and grants directly to Ukrainian firms to produce equipment within Ukraine. Using this model, Denmark has become Ukraine’s largest sponsor by percentage of GDP, and for their part, the Ukrainians couldn’t be happier. In January, then Ukrainian Prime Minister Denys Shmyhal (currently Ukraine’s defense minister) told the Rada he hopes to see $1 billion raised by the Danish Model by the end of this year. The initiative has led to a massive expansion of Ukraine’s defense industrial capacity, which the Ukrainians are planning to reach $35 billion in 2025. If they hit their target, Ukraine will challenge the UK, France, Germany, and Italy as the top defense producer in Europe.

Denmark benefits from this arrangement in two major ways. First, as a net contributor to the EU, it has been allowed to organize collective EU expenditures under the Danish Model, but count them towards its own spending target for NATO’s 5% of GDP defense goal. In addition to allowing the Danes to avoid spending their own money, this allows them to sidestep large investments in domestic military manufacturing, eliminating the risk of building a military-industrial complex from scratch when that complex may become superfluous if the war ends.

Second, Danish firms have been incentivized to create joint Danish-Ukrainian ventures in Ukraine, with the government subsidizing up to 70% of startup costs. These joint ventures rely on Danish management, creating high paying corporate jobs, while the burden of construction and manual labor leverage low Ukrainian labor costs. Labor in Ukraine is as little as 1/10th the cost of Danish labor.

These joint ventures don’t just go one way, as certain Ukrainian companies have been allowed to accept partial Danish ownership in exchange for establishing offices and production lines within Denmark. This is both an extension and inversion of the Danish model, as Ukrainian firms take on the debt, which is issued by the EU, and in turn invest in infrastructure within Denmark, rather than placing a purchasing order. This minimizes Danish risk.

Under this alternative model, Ukrainian firms have spun up production lines for drones and repair facilitates for air defense radars. The largest deal of this kind so far comes from Fire Point, the Ukrainian drone manufacturer currently embroiled in a corruption scandal, which plans to make rocket fuel for missiles on Danish soil.

Denmark isn’t the only country to work under this framework. Rheinmetall has established repair facilities for their armored vehicles in Ukraine, and has attempted to open an artillery shell plant there, though this initiative has made little progress since being announced in 2024. Saab, KNDS, Colt CZ, and FFG have announced similar projects. Turkey’s Baykar has thus far been the only firm to establish a major defense production plant on Ukrainian territory, but the $100 million facility was largely destroyed by a Russian strike in August, before it could come online.

The wisdom of opening a large defense plant in a country under constant attack from a vast suite of Russian standoff munitions is questionable, which may explain why plans to do so face extensive delays. But it’s still useful to interrogate why European defense contractors are so enthusiastic about pouring money into Ukraine.

The conceptual basis for all of the Danish Model, according to the Danes, is turning Ukraine into the “arsenal of Europe.” After a Ukrainian victory or stalemate, European defense companies and joint EU-Ukraine defense ventures would relocate their production to Ukraine, taking advantage of rock-bottom labor costs and stringent regulations imposed on the Ukrainian government and economy by the IMF and World Bank as loan conditions. These conditions were designed to benefit the EU.

In this universe, Ukraine would become the center of European weapon production, and perhaps manufacturing in general. High labor costs and social benefits in the EU proper limit profit margins, even in the distorted world of defense. Ukraine, with its government and economy under the thumb of institutions like the IMF, could be made to import millions of migrant laborers from countries like India, keeping labor costs low while compensating for the demographic crisis caused by the war. Think tanks like EasyBusiness have already outlined the number of workers needed and the regulatory process for importing them. European conglomerates and majority European-owned joint ventures would reap the rewards.

Dirty Tricks

In the meantime, Ukraine is a military-industrial wild west. Firms like Fire Point, which only a few years ago was a casting agency for TV production, have secured billions in defense contracts. The bidding process for government contracts – typically backed by European cash – is opaque and rife with corruption. Production rates are shrouded in secrecy, and facilities are constructed in secret locations. Dozens of major Ukrainian defense contracts have been awarded to companies that place the highest bids, implying corruption. Payments are made for weapons that are never delivered. Huge overpayments are common. International arms dealers are awarded billion dollar contracts they have no ability to fill.

Several European defense companies have been caught up in corruption scandals related to supplying arms to Ukraine. Denmark has supplied hundreds of millions of dollars to Fire Point, which now stands accused of falsifying its production rates of drones and the beleaguered FP-1 “Flamingo” cruise missile. The firm received nearly 10% of Ukraine’s domestic defense procurement budget in 2024. Danish Defense Minister Troels Lund Poulsen has publicly defended the partnership.

Similar corruption scandals have mired Polish firm PHU Lechmar – the beneficiary of a highly suspect €553 million artillery shell contract from the Ukrainian Border Guard – and the Czech STV Group, which resold Turkish shells to Ukraine at massively inflated prices. In 2022, Ukrainian arms dealer Lviv Arsenal conspired with Ukrainian MoD officials to embezzle $40 million through a fraudulent deal for mortar shells. The Ukrainian government money, a 97% upfront payment – the standard ceiling for such deals is 50% – moved from Lviv Arsenal through a series of shell companies in Slovakia and Croatia before disappearing. The mortar shells, marked up nearly 100% over the market rate, were never delivered. In August, an $11 million scheme involving Ukrainian parliament members, regional government officials, the Ukrainian National Guard, and an unspecified domestic drone manufacturer was uncovered by the National Anti-Corruption Bureau.

This form of petty corruption is of little benefit to European defense conglomerates with market caps approaching $100 billion, but an environment in which such corruption is tolerated is one where more ambiguous forms of graft and bribery can thrive. Even in the tightly regulated EU, corruption is rampant. Millions of euros in bribes paid in exchange for billions worth of deals by distinguished European defense contractors like Airbus, BAE Systems, Dassault, ThyssenKrupp, and even Rheinmetall have been uncovered in recent years. In the global arms industry, corruption is the norm rather than an aberration.

Each of these defense contractors is directly involved in procurement deals with Ukraine. These companies have operated for decades in an era of relative peace in Europe, and the war presents in a once in a generation opportunity. By forming joint ventures with Ukrainian firms, they can hit the ground running with the requisite Ukrainian connections to secure favorable contracts from the Ukrainian government, which acts a central hub into which unprecedented sums of public money are flowing from Europe, then back out again. While corruption may be commonplace in the EU proper, it’s the core reality undergirding the entire Ukrainian project. Far from the watchful eyes of European regulators, the EU military-industrial complex is having a field day.

Dividends

Without the massive surge in defense spending, the German economy would have posted a net decline in GDP since 2022, instead of extremely modest 0.2% growth. For the EU as a whole, defense spending has accounted for as much as 20% of growth since 2022. While the contribution to GDP from the defense sector is still small, much of this is the result of the cruel bargain staked out between the US – which set the 5% GDP defense spending target – and other NATO member states. The EU is still importing the majority of its military products, heavily benefiting the US and non-EU states like Turkey.

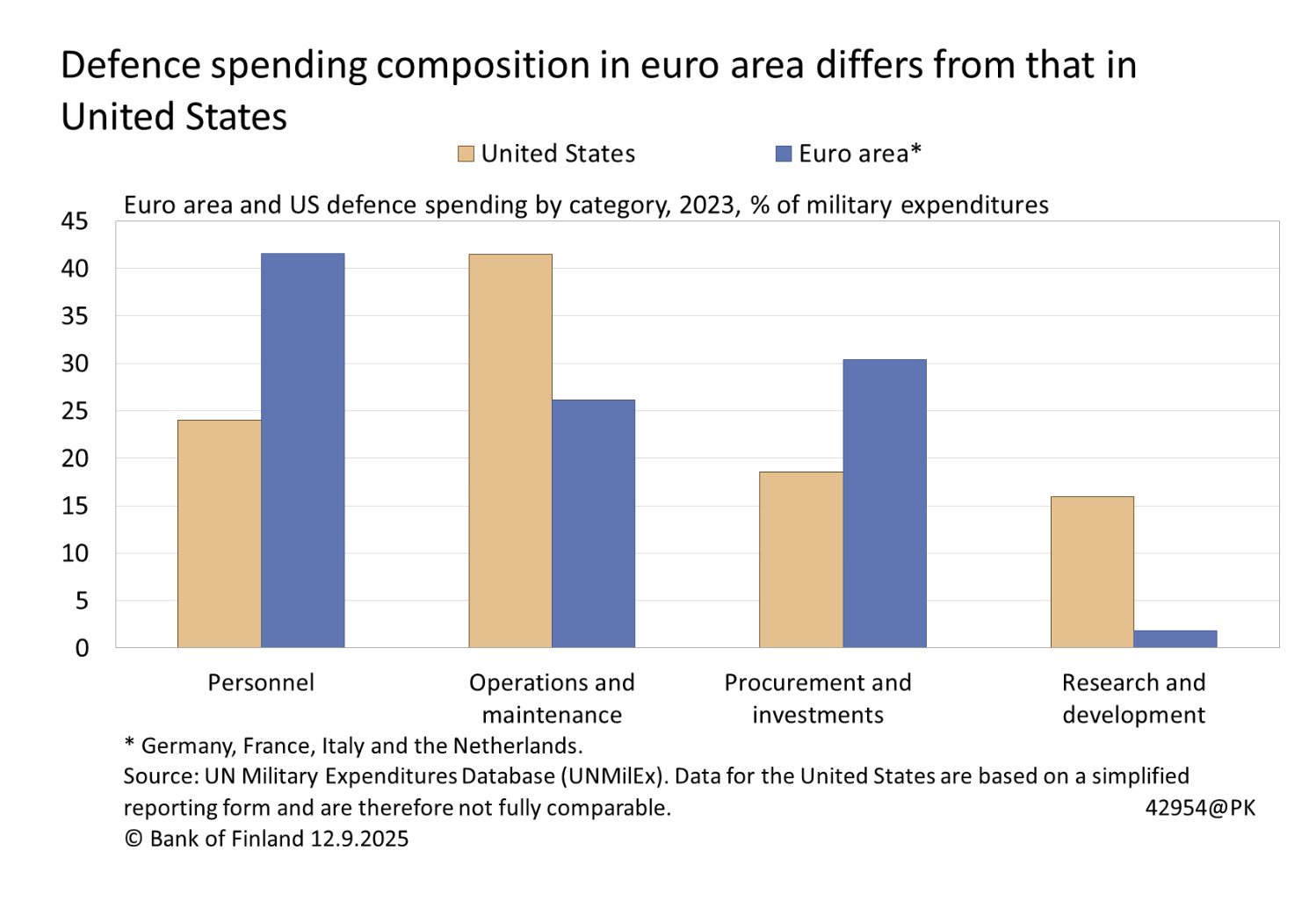

But future EU plans aim to correct this. In economic policy, the effect of public spending is measured by its multiplier effect – a multiplier of one means that for every Euro spent, a Euro is added to GDP. A multiplier less than one implies that for every Euro spent, less than a Euro in total output is generated. Military spending typically has a lower multiplier (below 1) than other types of spending, like infrastructure projects. In order to achieve the highest multiplier possible, defense spending is ideally spent on high tech R&D, rather than on personnel. The Europeans currently spend much more on personnel than they do on research and procurement.

Ukraine represents an opportunity to change this. European-owned ventures providing weapons to Ukraine can effectively generate their own demand, by lobbying their own governments to issue new debt to fund procurement deals. Much of the spending in the beginning phases of the war went towards procuring existing systems, rather than researching new ones. But the Danish model envisions Ukraine as a vast laboratory for European defense contractors. As European-Ukrainian joint ventures convert vast sums of R&D money into weapons, they can be tested in the field immediately, and then sold around the world.

After several years of new industrial projects, up front construction costs can now be paid off through regular operations. And defense expenditures haven’t even reached half of the European target yet. The biggest negative impact on the European defense spending multiplier is the percentage of that spending that goes towards imports, because they add to the exporter’s GDP, rather than Europe’s. But the share of spending going towards imports is steadily beginning to fall.

There are several issues with the European plan. Public spending funded by tax increases tends to permanently lower the multiplier effect of that spending, while debt financing will increase a multiplier temporarily. But if a country’s debt-to-GDP ratio gets too high, or servicing the debt becomes a burden, the multiplier can become negative. Historically, defense spending has been financed with increasing public debt, and that’s the plan for Europe. This summer, the European Council activated a provision in the Stability and Growth Pact called the national escape clause that will allow 15 member states to exceed the normal EU limit for deficit spending. The war in Ukraine and the need for increased spending were cited as the rationale.

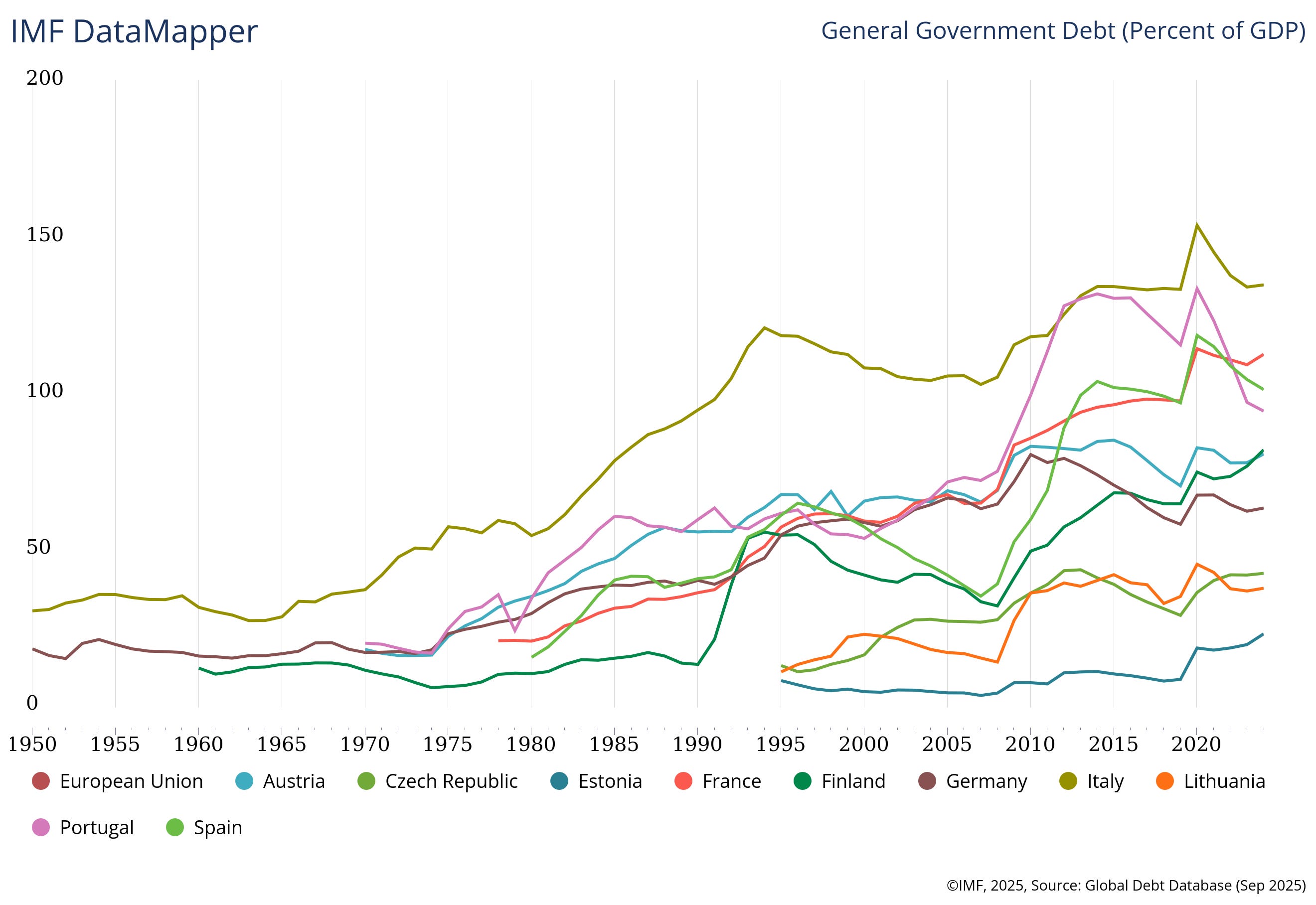

Taking on excessive debt to fund defense, and in turn stimulate the EU economy, is a form of kicking the can down the road. Italy, France, Belgium, and Spain have surpassed 100% debt-to-GDP ratios, while Portugal, Austria, Hungary, Poland, and Slovakia are being observed under the EU’s Excessive Deficit Procedure for their deficit spending. The UK’s ratio stands at 103%, and Germany’s ratio has increased by a massive 25% this year alone. With the German economy stagnant, and the multiplier effect of defense spending well below one, the Europeans are digging themselves into a long term hole.

Defense sector gains have been major. The sector’s weighting as a percentage of the overall European market has tripled since 2022, outperforming the market as a whole by a factor of six. But the average European hasn’t seen the benefits. Defense employs around half a million people within the EU, but employment gains have been modest, adding around 50,000 jobs. Meanwhile, traditional manufacturing has been plagued by losses of over a million manufacturing jobs over the last five years. Germany alone has lost 600,000 manufacturing jobs since 2022.

At best, the European defense spending strategy seems to offer a way to maintain stagnation, rather than achieve growth. But outside of economic concerns, it’s functioned as an ingenious political solution. Rather than dealing with the EU’s economic problems head-on, the Union’s governments have been able to launder a massive economic stimulus plan as a solution to a violent external threat. A courageous facade has been erected to cover clinical – and probably irresponsible – fiscal policy. Appealing to morality, ideology, and fear has been widely successful, and European populations have mostly accepted the messaging.

Because of this, it’s highly unlikely that the EU will tolerate an early conclusion to the war in Ukraine. They stand to lose the justification for their spending, lucrative contracts for their defense sectors, tens of billions on loans that Ukraine will be unable to pay, and the massive investments they’ve made into military-industrial infrastructure. Their dream of a generational extractive project in the form of a debt-ridden, prostrate Ukraine, a place outside the EU but with every trade and economic agreement written solely to benefit it, stands at risk of being destroyed by a steadily advancing Russian army.

Anything less than a permanent war footing could potentially spell disaster. If Ukraine or the NATO spending project collapses, expect major upheaval across the continent.

There will be no Ukraine in a few years. Every penny “invested” that doesn’t get kicked back under the table may as well be lit on fire, and by forcing Russia to develop a symmetric capability far from the conflict zone that cannot be destroyed by any weapons that Europe has or could hope to have they are creating a massive power differential that can only end with yet another stunning defeat once the time comes for Europe to actually attack.

And attack they will. The result will be the same as every other time: total defeat and another century of hate culminating with yet another suicide by cop. They are incapable of backing down because it will mean the end of these politicians.

Expect continuous “accidents” at these new facilities. And in Ukraine the Russians will wait until the full investment has been made and the plant is about to produce a finished product and bomb it to dust with all of the skilled laborers inside. Anyone underwriting these loans is a fucking idiot, and that pretty much describes Europe these days.

Super good analysis